The 50-Year Mortgage: Debt Slavery or Decent Idea?

Calm down, TikTok. You weren’t paying off that 30-year loan anyway.

I KNOW. IT’S LATE. I woke up at the usual unholy hour of 4:30 a.m. to no internet—not to mention some disturbing error messages. After an area-wide outage was confirmed, I spent the better part of the day cleaning, making soup, and trying not to curse. (Result: I cleaned and made soup.)

Anyhow, service was just restored and I thought about holding this post until tomorrow, but I am proud of my never-missing-a-day record, so hopefully this will reach some eyeballs and not confuse anyone too terribly. Thanks to those of you who reached out to check on me. I was happy to know I was missed. ;)

And now, for today’s feature presentation…

Just when you start to think we might get a 24-hour break from the political dumpster fire that is the mediasphere, Trump tosses a fresh grenade into the news cycle. To address the country’s undeniable housing unaffordability crisis, the real estate tycoon-in-chief floated the idea of a 50-year mortgage.

WHAT TRUMP ACTUALLY SAID: What if there was an option—some people call it a BRILLIANT OPTION, and maybe it is, really—of adding a few months to people’s payouts so more of them could afford houses? So I said, maybe that’s something we should look into.

WHAT THE TRIGGERED MASSES HEARD: Don’t let Radical Left Lunatic Democrats fool you into paying off your homes. FIFTY-YEAR MORTGAGES are what all Americans need, NOW! The Best in the World, believe me. No matter what the Fake News says, I am going to MAKE MORTGAGES GREAT AGAIN!

As you might imagine, the internet is having a full-body meltdown, as if someone suggested we all serve herb-roasted crickets on Thanksgiving. People are screaming “IT’S DEBT SLAVERY!” and “THIS IS LITERALLY INDENTURED SERVITUDE!” and calling the very concept “A DISGUSTING INSULT!” with the kind of panic normally reserved for killer hornets or the Starbucks holiday cup drop.

I get it. On paper, a 600-month mortgage looks like a lifetime commitment with all the fun of a root canal but with fewer drugs. The charts make it seem like you’ll be 97 years old, hunched over your walker, mailing in that final payment with a shaky hand and a note that says, “I HOPE YOU’RE HAPPY, YOU BASTARDS.”

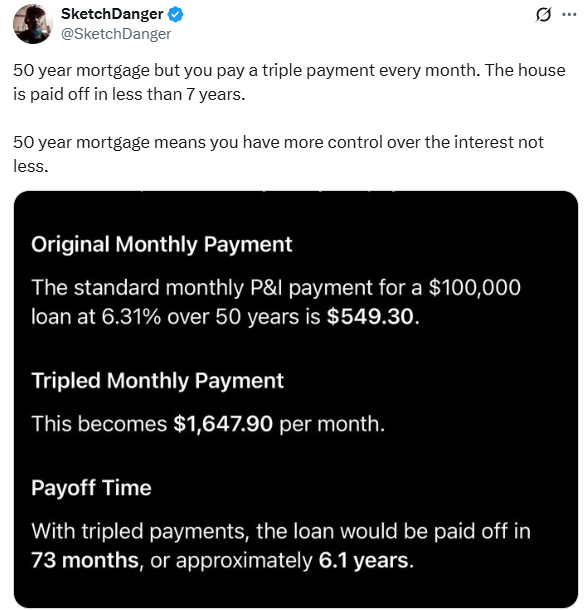

But here’s the secret economists don’t bother mentioning because it would ruin half of social media’s moral outrage economy: almost nobody pays off their mortgage, ever, period. The average American swaps homes (and loans) every 7–10 years. A huge chunk of the country refinances every time a bank waves a free toaster at them. People move, modify their payment plans, divorce, upgrade, downsize, or flee to Tennessee because New York is descending into communism. What the masses actually need is breathing room in their monthly budget—something longer terms can provide. You still build equity (which you don’t get from renting), you still benefit if rates come down, and you’re still free to pay the thing off early like a responsible adult. Calling this “economic genocide” while Blackstone is buying entire ZIP codes and renting them back to the middle class feels a bit… selective.

The truth is, most people treat mortgages like marathons they signed up for when they were drunk—something they could technically complete, but few ever do. So the idea that a 50-year mortgage “traps you for life” is adorable, because most of us were never getting out of our bank-loan relationships anyway.

And here’s where I think people are missing the plot: a longer mortgage doesn’t lock you into debt; it just lowers the monthly payment so you can actually get into a house in the first place. You know—ownership. Equity. Wealth-building. All that stuff financial gurus on TikTok howl about while selling you a $499 “budgeting course” filmed in a rented Airbnb. (And yes, I know that mortgages frontload interest… but as someone who’s made far more money buying and selling homes than filing W-2s, I also realize that homes generally appreciate faster than inflation—sometimes exponentially. Thus, equity.)

The other thing the internet is ignoring is the core philosophy of debt as a financial tool. Imagine you owe $500K on your house and you win a $500K scratch-off tomorrow. You could pay off your mortgage… or you could use that money to buy another property, let renters cover the new note (or yours, if you pay cash for the new pad), and walk away with two appreciating assets instead of one.

You could also pick up a couple of vending machines and let sugar addicts fund your retirement. Invest in equipment that turns your side hustle into an actual income stream. Buy some boring business that spits out money like an ATM.

Gurus like Grant Cardone and Robert Kiyosaki say never pay off your mortgage—leverage it. Cheap, fixed debt is a tool, not a trap, one investors use to stockpile wealth while everyone else is just trying to get to the last coupon in the payment book.

[*Explains to iGeneration children that yes, mortgages once came with an actual coupon book—that’s literally what it was called—and you would tear one out and send it off in the mail each month with your paper check like a pioneer woman, because that’s what you did back in the nineteen hundreds.]

If you’re going to be trading your dollars for shelter until your kids are old enough to put you in a nursing home anyway, you might as well be paying into something you partially own instead of funding your landlord’s third boat. A 50-year mortgage doesn’t magically make you a serf; it just spreads out the cost of the castle so you can, you know, have one. And unlike renting, it comes with built-in “forced savings”—every payment quietly stuffs a little equity into your proverbial mattress. Plus, people take care of what they own; no one upgrades the kitchen in an apartment they’re one leaky faucet away from losing. But give someone even a sliver of ownership, and suddenly they’re installing dimmers, repainting cabinets, and Googling “is crown molding worth it?”

It’s worth pointing out that back in the day, a 30-year loan was considered insanity—at least, until it was credited with “saving the housing market”. Before the 1930s, buying a house meant coughing up half the price in cash, paying interest-only for a few years, and then praying you won the lottery before the giant balloon payment dropped like a cartoon anvil. (If you didn’t have the down payment, you either rented for life or sold your soul to a loan shark—basically the equivalent of choosing between anesthesia-free surgery or dying of scurvy.)

FDR swooped in during the Great Depression and invented the 30-year mortgage so everyday people could stop refinancing every time Mercury went into retrograde. Banks whined that 30 years was “way too long”—and then quietly made fortunes on it. Meanwhile, most of the world still uses 2–5-year reset mortgages that act like a clingy ex who changes their mood (and your payment) every few months. So honestly, stretching to 50 years isn’t financial witchcraft; it’s the logical next step in America’s long tradition of turning terrifying debt into a cozy monthly hug.

Are there downsides to adding a few decades to your home loan? Sure. Housing prices could inflate faster than a bachelorette bar tab in Nashville. Developers will absolutely use this as an excuse to list a 600-sqare-foot studio for “a reasonable $1.3 million.” And yes, if you somehow stay put for the full 50 years, you’ll pay enough interest to personally bankroll the bank president’s beach house.

But again: when’s the last time someone you know lived in one home for half a century? Grandma doesn’t count—she bought that house for $18,000 in 1962 and refuses to leave because her kitchen still has the original avocado-green stove and “they just don’t make appliances like that anymore.”

(She’s not wrong, incidentally.)

The real choice isn’t between a 30-year mortgage and a 50-year mortgage. It’s between renting forever or getting on the equity ladder at all. Critics act like the alternative is some affordable dream house in a walkable neighborhood with a yard and a view, when in reality it’s a crappy rental with rising rent and zero skin in the game. And if a longer term is what lets the Costo-card crowd enter the market instead of doomscrolling Zillow like it’s The Hunger Games for homeowners, then maybe—just maybe—the idea isn’t the harbinger of financial hell the think-piece architects want it to be.

TikTokers whine endlessly about how homeownership has been ripped from their grasp, and wax poetic about how much easier it was for previous generations. But was it? Because last time I checked, our parents and grandparents didn’t live the way we do. They didn’t have a flatscreen TV in every room and the latest iPhone upgrade every year and a house full of Pottery Barn furniture and emotional-support tchotchkes from HomeGoods. They lived in crappy houses. They scrimped. They saved. They cooked at home. They clipped coupons. They didn’t take exotic vacations. They spent less for an entire year’s worth of coffee than we spend on a single Starbucks run. They bought cars they could afford and drove them into the literal ground. They darned their socks when they got holes in them instead of replacing them. Spoiled, they were not.

Gen Z: Are scrimping and darning, like, actual things?

When I was born, my family was living with my aunt and uncle in their two-bedroom house (there were five of us, including three kids under three, in that place—thanks again, amazing Aunt Linda and Uncle Jack!) while my dad and uncle built us a house. My grandparents made it to their mid-nineties without ever knowing the luxury of a dishwasher. The folks who eventually crossed the homeowner finish line (and weren’t trust-funders) lived beneath their means—an ancient ritual the Retail Therapy Generation seems to consider a hate crime.

At the end of the day, housing is expensive (whether you rent or own). So yes, worry about affordability. Stress over inventory. Be outraged about interest rates and illegal immigrants driving up prices and private equity firms snapping up the best deals. Maybe take stock of your spending habits, if you’re feeling bold. But freaking out because some families may get more options instead of fewer? Please. Most of us treat our 30-year mortgage like a seven-year situationship anyway.

Am I way off base? I’m sure you’ll let me know in the comments. ;)

I can personally attest to an amazingly clean home, delicious smells coming from the kitchen and a day full of really bad language coming from every corner of my home.

You made it honey.

One of my many careers was Mortgage Loan Broker. Agree with you 100%. Especially that it will enrich communities because Pride of ownership kicks in. People pay off mortgages early all the time for various reasons, even if they don't move. And lowering the cost of entry will help many.